Sundry Photography/iStock Editorial via Getty Images

IBM (NYSE:IBM) is scheduled to announce Q4 earnings results on Wednesday, January 25th, after market close.

The consensus EPS Estimate is $3.61 (+7.8% Y/Y) and the consensus Revenue Estimate is $16.38B (-1.9% Y/Y).

Over the last 3 months, EPS estimates have seen 4 upward revisions and 2 downward. Revenue estimates have seen 2 upward revisions and 2 downward.

The tech giant last posted Q3 results that topped Wall Street’s estimates, and suggested that sales are going to improve next year.

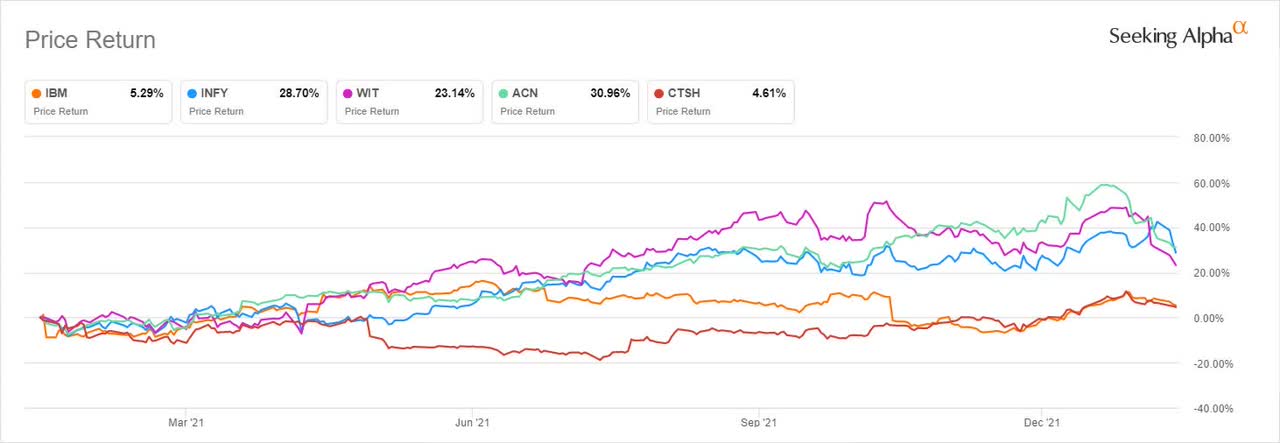

Ahead of the Q4 results, MoffettNathanson upgraded IBM citing potential for strong IT services growth this year, despite – and in some cases even because of – recession concerns. The stock has handily outperformed the S&P 500 in the past year.

Credit Suisse is also bullish on the stock, given its strong software portfolio (AI, security), ongoing mainframe refresh and improving currency environment. Demand appears to have held up well in Q4 according to its analysts, but investors will be focused on 2023 cash flow projects as IBM targets revenue growth and customer acquisition.

Stifel expects revenue growth plans to continue to chug along in 2023 as well, although software/consulting sales will likely slow with economic growth.

On the other hand, Morgan Stanley sees revenue growth decelerating and a risk of underperformance in H2 2023, even as the stock closed 2022 as the best performing name in its IT hardware coverage.

Seeking Alpha’s quant systems, which historically outperforms the stock market, has a hold rating on IBM’s shares.

Over the last 2 years, IBM has beaten EPS estimates 100% of the time and has beaten revenue estimates 75% of the time.

{kind=link}