Natee Meepian/iStock via Getty Images

U.S. property/casualty insurers’ underwriting results are expected to improve this year on the back of higher premium rates in underperforming automobile and property segments, according to ratings agency Fitch.

However, claims volatility amid higher inflation and broader macroeconomic uncertainty could hinder a return to underwriting profitability in 2023.

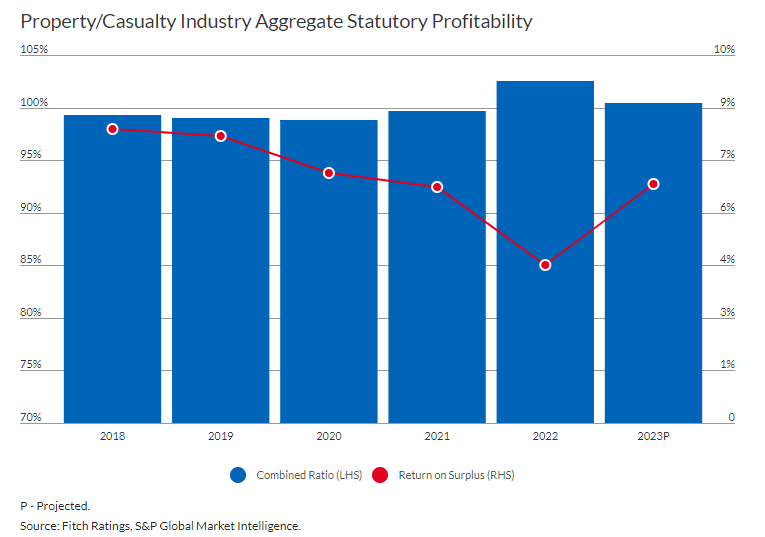

Fitch has a neutral outlook on the property/casualty insurance sector, based on stable to improving operating performance this year. It forecasts a 100.4% industry combined ratio for the year.

Personal lines will likely improve in 2023, given recent pricing and underwriting adjustments amid normalizing insured catastrophe losses. Commercial lines overall combined ratios are expected to worsen slightly from current favorable underwriting profit levels.

Direct written premiums growth will slightly moderate, but remain higher than historical norms on strong momentum in personal lines premiums. Direct written premiums grew over 9% for the second straight year in 2022, helped by commercial and personal lines rate increases.

Return on surplus fell for the fourth year in a row in 2022 to 4.3%, but is expected to rebound this year. “Variability in natural catastrophe losses remain concerning, compounded by sharp increases in reinsurance costs and less reliable available capacity,” Fitch cautioned.

Note that the SPDR S&P Insurance ETF (KIE) gained 4.8% in the last six months, but underperformed the 6% gain in the Select Sector SPDR Financial ETF (XLF) and the 15.1% increase in the S&P 500 index.

Earlier this year, S&P Global Ratings revised its view on the U.S. property/casualty insurance sector to negative, as a result of declining investment values and weaker underwriting results. It expects weaker credit trends to continue this year.

{kind=link}