Quick Answer

To decide on buying your leased car, compare its residual value (e.g., $15,000) with its current market value (e.g., $17,500). Consider the car’s condition, potential repair costs, and your emotional attachment. Check prices of similar cars in the market and factor in additional costs. Remember, you might be able to negotiate the buyout price with the leasing company.

Key takeaways:

Determine the Residual Value: This is the amount the leasing company has predetermined your car will be worth at the end of your lease. It’s the purchase price if you decide to buy the car. For example, let’s say your leased car’s residual value is $15,000.

Assess the Current Market Value: Check websites like Kelley Blue Book, Edmunds, or NADA to determine the current market value of your car. Suppose you find out that the market value is $17,500.

Compare Residual to Market Value:

If the residual value ($15,000) is less than the market value ($17,500), then buying your leased car can be a good deal since you’re essentially getting a $17,500 car for only $15,000.

If the residual value exceeds the market value, you might be overpaying if you decide to buy the car.

Evaluate the Car’s Condition:

Under Mileage: If your car has fewer miles than allowed in the lease, it might be to your advantage. For example, if you were allowed 36,000 miles over 3 years and only drove 30,000, your car may be worth more than similar models in the market.

Wear and Tear: If your car has excessive wear and tear, you might face penalties if you return it. If damages are more than what’s considered “normal wear and tear”, it might be cheaper to buy the car rather than pay hefty fees.

Consider Future Costs:

Maintenance: If the car is out of warranty and you expect significant repairs in the near future, factor in those costs. For instance, if you expect to spend $2,000 on repairs in the next year, add that to the cost of buying out your lease.

Financing: If you don’t have cash to buy the car outright, consider interest rates on a car loan.

Evaluate Emotional Factors:

Attachment: If you love and feel firmly attached to the car, this could favor buying it.

Peace of Mind: Knowing the car’s entire history can give you peace of mind versus buying a used car with an unknown history.

Compare with Alternatives:

Research the cost of a similar new or used car in the market. If a similar used car costs $18,000 and a new one is $25,000, buying your leased car for $15,000 might seem like a better deal.

Don’t forget to factor in registration, taxes, and other fees associated with getting a different car.

Negotiate: Sometimes, the leasing company may be willing to negotiate the buyout price, especially if they believe you might return the car and they’d incur costs to resell it.

Consider the Residual Value and Purchase Price

The residual value is the estimated value of the car at the end of the lease term. It is calculated as a percentage of the manufacturer’s suggested retail price (MSRP). The percentage depends on multiple factors:

Car’s make and model

Lease term

Mileage allowance

Current market conditions

The higher the residual value compared with MSRP, the better for the lessee, as it means lower monthly payments. For example, if the car has an MSRP of $30,000 and a residual value of $15,000, and the lease term is 36 months, the monthly lease payment will be $416.67 ($15,000/36=$416.67)

If the residual value was higher, $20,000, for example, the depreciation amount would be $10,000, so it means that monthly lease payments would be $277.78.

This is because the lessors are more likely to be able to sell the car for at least the residual value at the end of the lease, which means they are less likely to lose money.

How Does Residual Value Influence Decision To Buy A Leased Car?

The residual value is the estimated value of the car at the end of the lease term. This value will be used to calculate the purchase option price.

If the purchase option price is higher than the current market value of the car, it might be a good decision to purchase the vehicle.

For example:

Residual value: $16,000

Purchase option price: $18,000

Current market value: $17,000

In this case, you would have to pay $1,000 more to buy the car at the end of the lease term compared with buying privately, but it will take you a lot of time, and you risk buying a car in worse condition, so it would be worth paying $1,000 more for the car you already drive.

To find out the market estimates, you should browse similar car listings on eBay Motors or Autotrader or use Kelley Blue Books car’s value calculator.

Evaluate Your Financial Situation

When you’ve considered the residual value and purchase price of your leased car, you also need to evaluate your financial situation.

1. Your monthly budget

Let’s say your car’s purchase price is $25,000, and you are planning to finance the whole amount. If your interest rate is 5%, your monthly loan payments, for a standard 60 months period, will be $500

If your monthly lease payments are higher than loan payments, it is wise to consider buying the vehicle.

Remember that financial experts recommend that car expenses, including insurance and fuel costs, should not exceed 10-15% of your monthly income. If your lease or loan payments are higher than this percentage, you should consider either leasing a more affordable vehicle or buying a used car that has lower monthly costs.

2. Down payment

If you have additional money, it is recommended to make a down payment to lower monthly payments.

A good rule of thumb is to put down 10% to 20% of the car’s purchase price. For a $25,000 car, this would mean a down payment of $2,500 to $5,000.

Difference between making a down payment vs. not making a down payment:

Option Loan amountInterest rateMonthly paymentTotal costNo down payment$25,0005%$500$3,000$5,000 down payment$20,0005%$416.67$24,999

As you can see, paying a down payment not only reduces monthly payments but also lowers the total cost of the vehicle by $5,000.

3. Insurance, maintenance & repairs

Another important factor to consider is if you will be able to allocate part of the budget for insurance, maintenance and repair costs.

You should budget at least 10% of the value of your car each year for these expenses. So if the car is worth $25,000, you should budget at least $2,500.

If you can’t ensure that you will be able to set asside extra money for the car’s maintenance, buying a car might be financially disadvantageous.

Appraise Car’s Condition and Mileage

The car’s wear and tear, as well as exceeded mileage, can significantly influence your decision to either keep leasing or buy the vehicle.

Leases usually come with specific limitations on the amount of mileage you’re allowed to use, and if you exceed these limits, it can result in costly fees. Most leases have a maximum mileage allowance of 12,000 miles per year. If you’re someone who drives extensively, you will be charged for each additional mile.

For example, if you lease a car with a 12,000-mile-per-year allowance and you drive 15,000 miles in a year, you will be charged 3,000 additional miles. The leasing company may charge you $0.15 per mile, so you would owe an additional $450.

Additionally, any wear and tear beyond what the leasing company deems as ‘normal’ can lead to penalties. The amount of additional payment varies depending on the car, the leasing company, and the extent of the wear and tear, but it is estimated that the average cost of wear and tear on a leased car is $1,200.

The most common items that are damaged in leased cars are tires, wheels, and the interior. How much it will cost you depends on the damage, but tires are the most expensive item to replace, with an average cost of $500, and the interior of a car is typically less expensive to repair, with an average cost of $200.

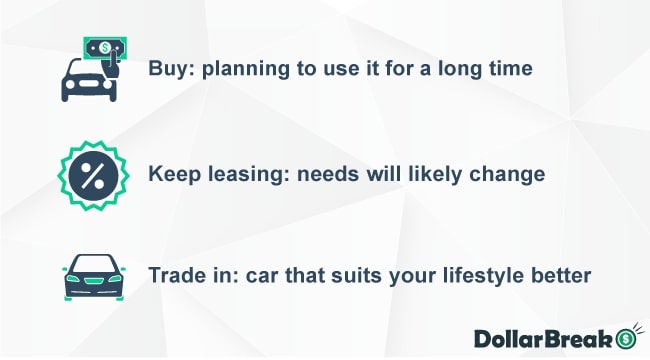

Your Future Plans

Your future plans and needs might also impact the decision to either buy a leased car or keep leasing.

If your current vehicle meets all your needs and you are planning to use it for a long time, buying the vehicle will allow you to build equity in the car over time, which could help you save money on your next car purchase, and you will have more control over the car’s maintenance and repairs.

If you predict that your needs will likely change, it is wise to either keep leasing or purchase a new vehicle that suits your lifestyle better. In this case, leasing will allow you not to worry about the maintenance and repairs and enables you to drive a new vehicle every 2 to 3 years.

If You Are Planning to Sell or Trade in the Car:

To find out if it is a wise decision to sell or trade in a vehicle, you should check current market values. Using tools such as the Kelley Blue Book car’s value calculator, you can estimate how much your car is worth and if you can sell it for a profit.

Keep in mind that selling privately can take you up to 52 days and will require at least 15 hours of your additional time. If you decide to trade in or sell the car online, the process will be much easier and faster, but you should not expect to earn as much as selling privately.

If you will be able to sell for a profit depends on multiple factors, such as your car’s make, model, mileage and demand. Check out similar car listings on eBay Motors or Autotrader to see the average prices of vehicles.

For example, if you buy a leased car for $25,000, but the current market value for such a car is $27,000, you can expect to earn $2,000 profit. However, in this case, you will be required to pay capital gain tax, which can cost you anywhere from $0 to $640.

Pros and Cons of Buying Your Leased Car

Buying a leased car at the end of your lease period has both its advantages and disadvantages. Here are some pros and cons to consider:

Pros of Buying a Leased Car:

• You know the Car – since you’ve been driving this car during the lease, you know the car’s history, how well it’s been maintained, if there are any issues and so on. When you feel confident and used to the car, driving can feel more relaxed and safer.

• No Over Mileage Fees – if you’ve exceeded the mileage limit marked in your lease terms, buying the car will help you avoid paying hefty over-mileage fees.

• No Wear and Tear Penalties – you might have to pay additional fees if the car has any damage beyond the “normal wear and tear”. Buying the car would allow you to avoid these penalties.

• Potential Bargain – if the purchase price of the car is less than the market value, it could be a good deal to buy it even if you are planning to sell it.

Cons of Buying a Leased Car:

• Higher Cost Over Time – buying out your lease highly likely will result in paying more in total compared to if you had bought the car outright initially due to lease fees and finance charges.

• Residual Value is Higher Than Market Value – If the residual value set in the lease contract is higher than the current market value, you will end up paying more than what the car is worth.

• More Financing or Cash Outlay – if you decide to buy the car at the end of your lease, you’ll either need to have the cash available to pay the buyout price or finance the balance, which could add more debt.

• Less Warranty Protection – the manufacturer’s warranty that often comes with a new car lease expires by the time you decide to buy, which means you’ll be responsible for any repair costs.

• Changing Technology – if you enjoy having the latest technology or safety features, buying your leased car means you’ll be missing out on any advancements that have come out since you started your lease.

FAQ

What if I don’t want to buy my leased car?

You have a few options:

• Return the car to the leasing company – schedule a pre-return inspection, where the leasing company will evaluate the car for any excessive wear and tear or mileage overages.

• Lease a New Car – start a new lease with the same or different car manufacturer or dealership. This allows you to constantly drive relatively new cars with the latest technology and safety features.

• Extend the Lease – some leasing companies might offer you the option to extend your lease if you’re not ready to make a decision yet. This could give you more time to decide whether you want to lease a new car, buy a car, or possibly buy your currently leased car.

What if I want to buy my leased car, but I don’t have the money?

In this case, you should get a lease buyout loan. The loan will be for the amount of the buyout price plus any fees or taxes. Good credit is required to qualify for a lease buyout loan.

If taking a loan is not an option, you should keep leasing until your financial situation allows you to buy the car or consider buying a used car from a private party.

When is it a good time to buy your leased car?

The decision to buy your leased car largely depends on your personal circumstances, but there are some conditions under which it may be a particularly good idea:

Lower Market Value

High Mileage or Excessive Wear and Tear

Good Vehicle Condition

Affordable Buyout Price

Satisfaction with Vehicle

Stable Future Use

{kind=link}