Updated on June 26th, 2026 by Bob Ciura

The goal of rational investors is to maximize total return under a given set of constraints.

The three components of expected return are:

Earnings-per-share growth

Dividend payments

Expansion/contraction of the valuation multiple

At Sure Dividend, we believe high-quality dividend growth companies represent the best stocks to buy-and-hold for the long run.

This is why we recommend stocks that have established track records of paying dividends, and raising their dividends over time.

Blue-chip stocks are established, financially strong, and consistently profitable publicly traded companies.

Their strength makes them appealing investments for comparatively safe, reliable dividends and capital appreciation versus less established stocks.

This research report has the following resources to help you invest in blue chip stocks:

This list contains important metrics, including: dividend yields, payout ratios, dividend growth rates, 52-week highs and lows, betas, and more.

There are currently more than 500 securities in our blue chip stocks list.

Even better, investors can maximize their portfolio return by purchasing quality dividend stocks when they are undervalued.

This article discusses the 10 best dividend stocks in the Sure Analysis Research Database currently trading within 10% of their 52-week lows.

The stocks are arranged by annual expected returns, in ascending order.

Table of Contents

The table of contents below allows for easy navigation.

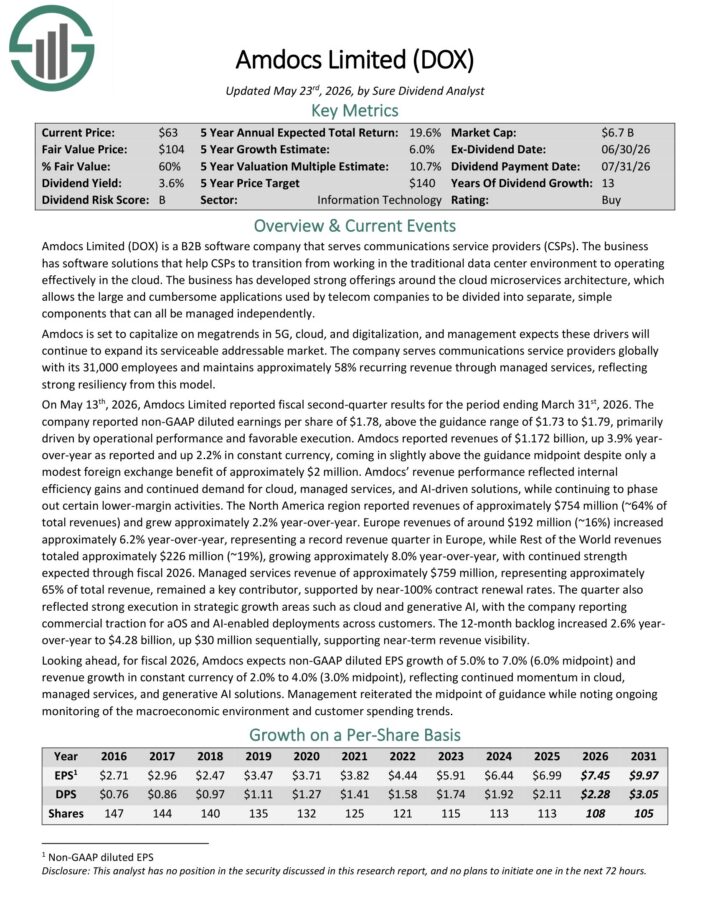

Beaten Down Dividend Stock #10: Amdocs Limited (DOX)

Expected Total Return: 25.1%

Amdocs Limited (DOX) is a B2B software company that serves communications service providers (CSPs).

The business has software solutions that help CSPs to transition from working in the traditional data center environment to operating effectively in the cloud.

The business has developed strong offerings around the cloud microservices architecture, which allows the large and cumbersome applications used by telecom companies to be divided into separate, simple components that can all be managed independently.

On May 13th, 2026, Amdocs Limited reported fiscal second-quarter results for the period ending March 31st, 2026. The company reported non-GAAP diluted earnings per share of $1.78, above the guidance range of $1.73 to $1.79, primarily driven by operational performance and favorable execution.

Amdocs reported revenues of $1.172 billion, up 3.9% year-over-year as reported and up 2.2% in constant currency, coming in slightly above the guidance midpoint despite only a modest foreign exchange benefit of approximately $2 million.

Amdocs’ revenue performance reflected internal efficiency gains and continued demand for cloud, managed services, and AI-driven solutions, while continuing to phase out certain lower-margin activities.

Looking ahead, for fiscal 2026, Amdocs expects non-GAAP diluted EPS growth of 5.0% to 7.0% (6.0% midpoint) and revenue growth in constant currency of 2.0% to 4.0% (3.0% midpoint), reflecting continued momentum in cloud, managed services, and generative AI solutions.

Click here to download our most recent Sure Analysis report on DOX (preview of page 1 of 3 shown below):

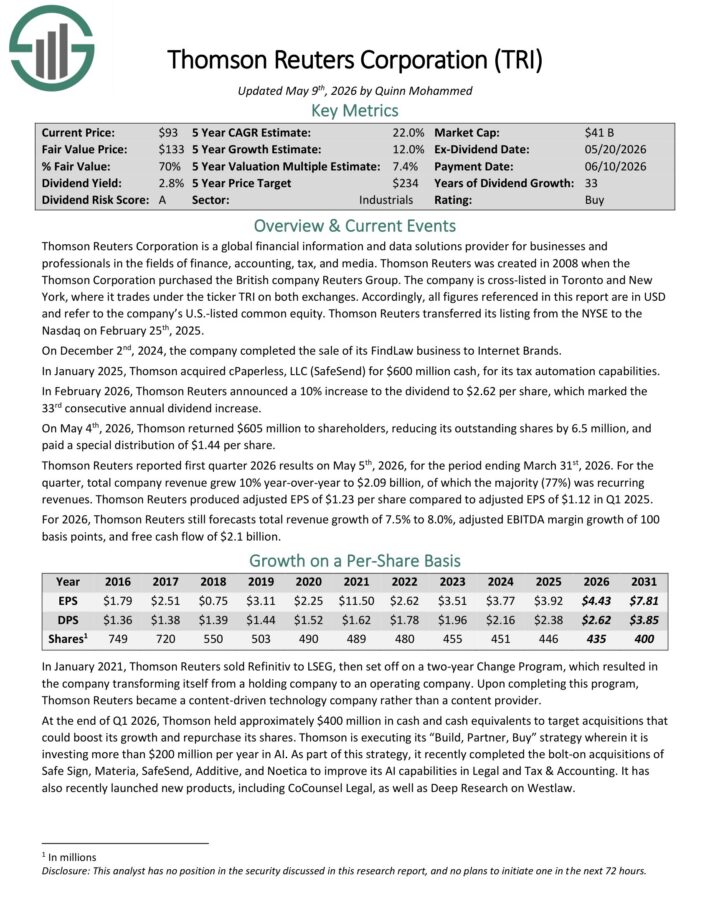

Beaten Down Dividend Stock #9: Thomson-Reuters Corp. (TRI)

Expected Total Return: 25.3%

Thomson Reuters Corporation is a global financial information and data solutions provider for businesses and professionals in the fields of finance, accounting, tax, and media.

In February 2026, Thomson Reuters announced a 10% increase to the dividend to $2.62 per share, which marked the 33rd consecutive annual dividend increase.

Thomson Reuters reported first quarter 2026 results on May 5th, 2026. For the quarter, total company revenue grew 10% year-over-year to $2.09 billion, of which the majority (77%) was recurring revenue.

Thomson Reuters produced adjusted EPS of $1.23 per share compared to adjusted EPS of $1.12 in Q1 2025.

For 2026, Thomson Reuters still forecasts total revenue growth of 7.5% to 8.0%, adjusted EBITDA margin growth of 100 basis points, and free cash flow of $2.1 billion.

Click here to download our most recent Sure Analysis report on TRI (preview of page 1 of 3 shown below):

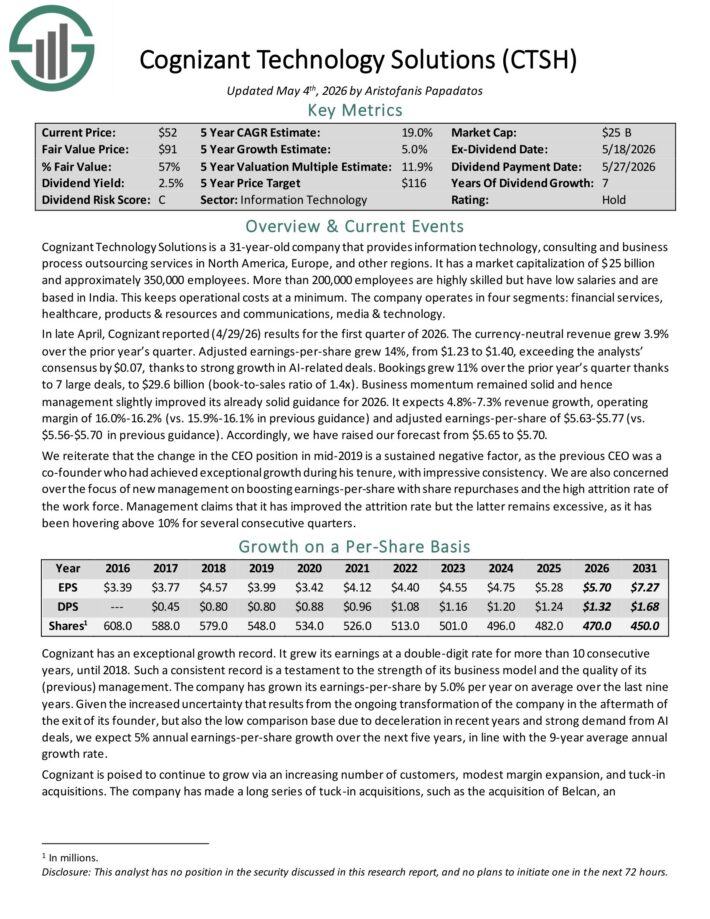

Beaten Down Dividend Stock #8: Cognizant Technology Solutions (CTSH)

Expected Total Return: 25.8%

Cognizant Technology Solutions is a 31-year-old company that provides information technology, consulting and business process outsourcing services in North America, Europe, and other regions.

The company operates in four segments: financial services, healthcare, products & resources and communications, media & technology.

In late April, Cognizant reported (4/29/26) results for the first quarter of 2026. The currency-neutral revenue grew 3.9% over the prior year’s quarter.

Adjusted earnings-per-share grew 14%, from $1.23 to $1.40, exceeding the analysts’ consensus by $0.07, thanks to strong growth in AI-related deals.

Bookings grew 11% over the prior year’s quarter thanks to 7 large deals, to $29.6 billion (book-to-sales ratio of 1.4x). Business momentum remained solid and management slightly improved its guidance for 2026.

It expects 4.8%-7.3% revenue growth, operating margin of 16.0%-16.2% (vs. 15.9%-16.1% in previous guidance) and adjusted earnings-per-share of $5.63-$5.77 (vs. $5.56-$5.70 in previous guidance).

Click here to download our most recent Sure Analysis report on CTSH (preview of page 1 of 3 shown below):

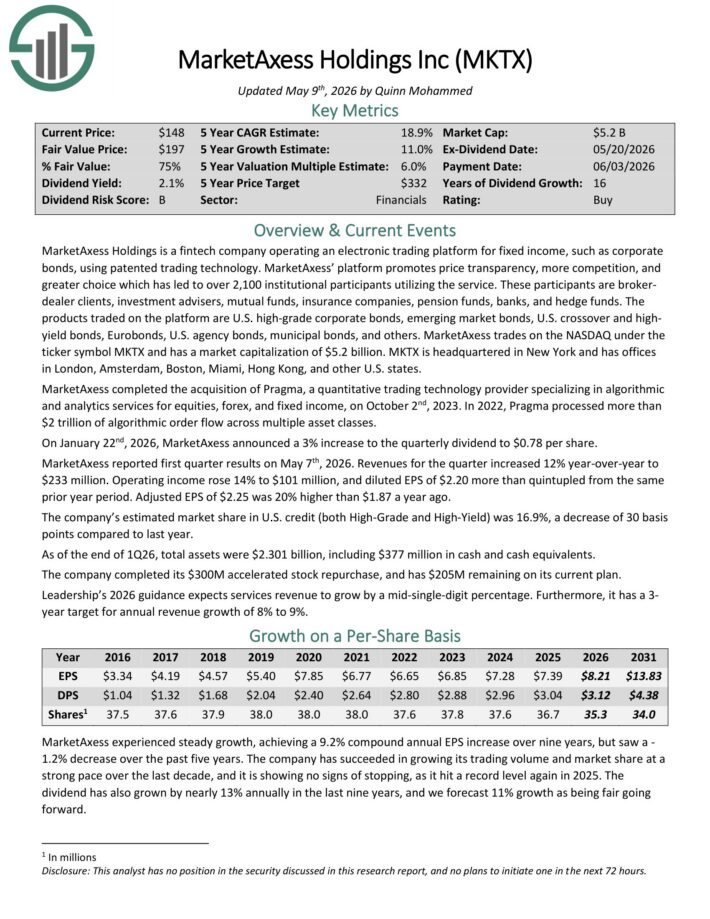

Beaten Down Dividend Stock #7: MarketAxess Holdings (MKTX)

Expected Total Return: 26.3%

MarketAxess Holdings is a fintech company operating an electronic trading platform for fixed income, such as corporate bonds, using patented trading technology.

MarketAxess’ platform promotes price transparency, more competition, and greater choice which has led to over 2,100 institutional participants utilizing the service.

These participants are broker-dealer clients, investment advisers, mutual funds, insurance companies, pension funds, banks, and hedge funds.

The products traded on the platform are U.S. high-grade corporate bonds, emerging market bonds, U.S. crossover and high-yield bonds, Eurobonds, U.S. agency bonds, municipal bonds, and others.

On January 22nd, 2026, MarketAxess announced a 3% increase to the quarterly dividend to $0.78 per share.

MarketAxess reported first quarter results on May 7th, 2026. Revenues for the quarter increased 12% year-over-year to $233 million.

Operating income rose 14% to $101 million, and diluted EPS of $2.20 more than quintupled from the same prior year period. Adjusted EPS of $2.25 was 20% higher than $1.87 a year ago.

Click here to download our most recent Sure Analysis report on MKTX (preview of page 1 of 3 shown below):

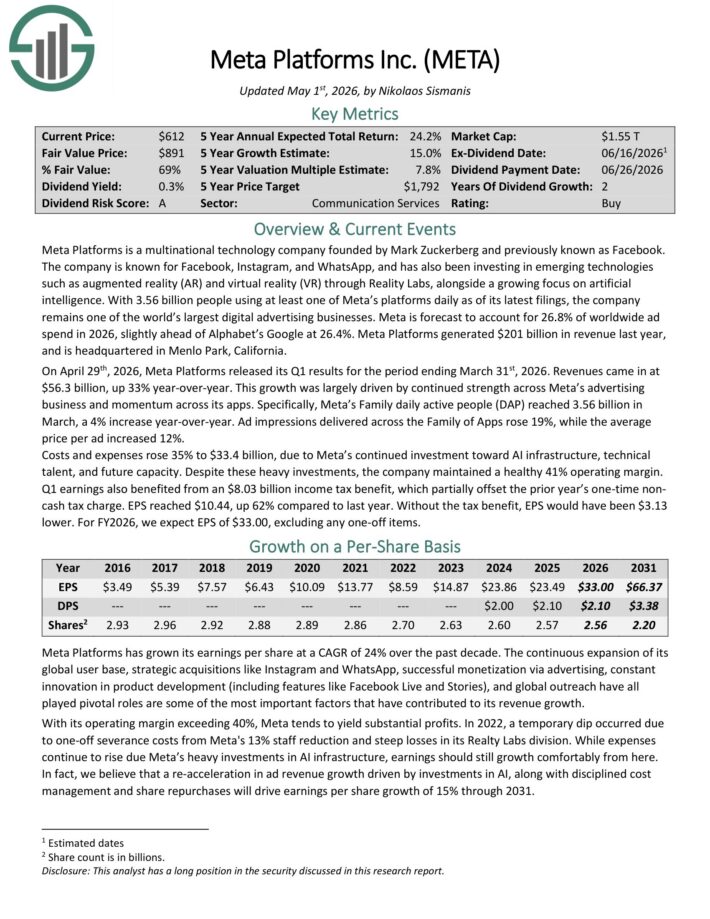

Beaten Down Dividend Stock #6: Meta Platforms (META)

Expected Total Return: 27.1%

Meta Platforms is a technology conglomerate known for its social media platforms, including Facebook, Instagram, and WhatsApp.

It has also been investing in emerging technologies such as augmented reality (AR) and virtual reality (VR) through its Oculus subsidiary.

With nearly 4 billion people logging into at least one of Meta’ platforms every month, the company attracts nearly 20% of all global advertising revenue, second only to Alphabet (GOOGL), which commands a substantial 40% market share.

Meta Platforms generates $201 billion in annual revenue, and is headquartered in Menlo Park, California.

On April 29th, 2026, Meta Platforms released its Q1 results for the period ending March 31st, 2026. Revenues came in at $56.3 billion, up 33% year-over-year.

This growth was largely driven by continued strength across Meta’s advertising business and momentum across its apps. Specifically, Meta’s Family daily active people (DAP) reached 3.56 billion in March, a 4% increase year-over-year.

Ad impressions delivered across the Family of Apps rose 19%, while the average price per ad increased 12%.

EPS reached $10.44, up 62% compared to last year.

Click here to download our most recent Sure Analysis report on Meta (preview of page 1 of 3 shown below):

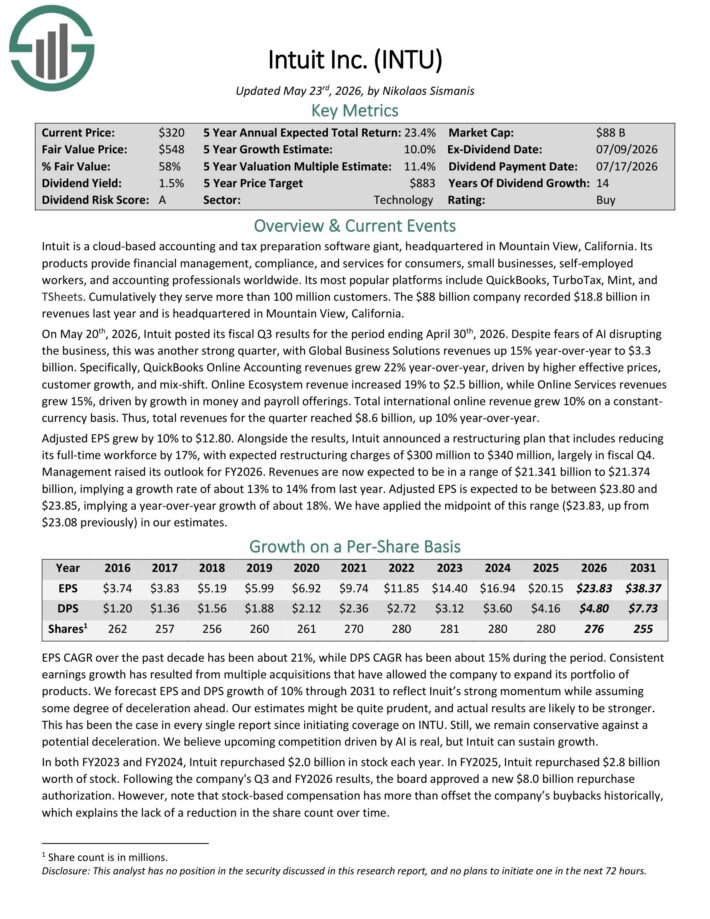

Beaten Down Dividend Stock #5: Intuit Inc. (INTU)

Expected Total Return: 29.0%

Intuit is a cloud-based accounting and tax preparation software giant, headquartered in Mountain View, California.

Its products provide financial management, compliance, and services for consumers, small businesses, self-employedworkers, and accounting professionals worldwide.

Its most popular platforms include QuickBooks, TurboTax, Mint, and TSheets. Cumulatively they serve more than 100 million customers.

The company recorded $18.8 billion in revenue last year and is headquartered in Mountain View, California.

On May 20th, 2026, Intuit posted its fiscal Q3 results for the period ending April 30th, 2026. Global Business Solutions revenues were up 15% year-over-year to $3.3 billion.

Specifically, QuickBooks Online Accounting revenues grew 22% year-over-year, driven by higher effective prices, customer growth, and mix-shift.

Total revenues for the quarter reached $8.6 billion, up 10% year-over-year. Adjusted EPS grew by 10% to $12.80.

Management raised its outlook for FY2026. Revenues are now expected to be in a range of $21.341 billion to $21.374 billion, implying a growth rate of about 13% to 14% from last year.

Adjusted EPS is expected to be between $23.80 and $23.85, implying a year-over-year growth of about 18%.

Click here to download our most recent Sure Analysis report on INTU (preview of page 1 of 3 shown below):

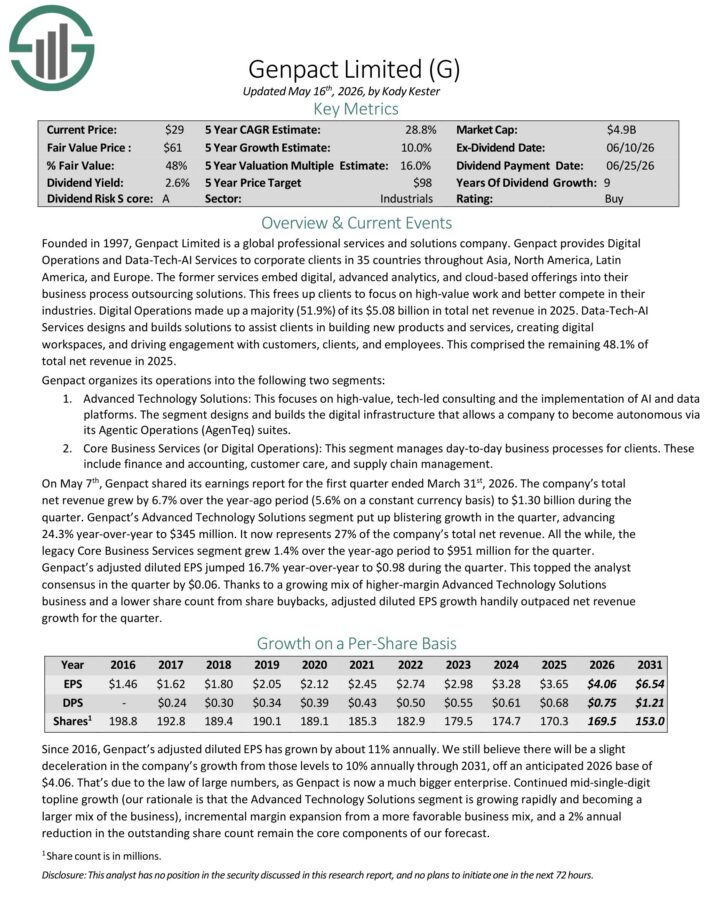

Beaten Down Dividend Stock #4: Genpact Limited (G)

Expected Total Return: 29.0%

Genpact Limited is a global professional services and solutions company. Genpact provides Digital Operations and Data-Tech-AI Services to corporate clients in 35 countries throughout Asia, North America, Latin America, and Europe.

The former services embed digital, advanced analytics, and cloud-based offerings into their business process outsourcing solutions. Digital Operations made up a majority (51.9%) of its $5.08 billion in total net revenue in 2025.

On May 7th, Genpact shared its earnings report for the first quarter ended March 31st, 2026. The company’s total net revenue grew by 6.7% over the year-ago period (5.6% on a constant currency basis) to $1.30 billion during the quarter.

Genpact’s Advanced Technology Solutions segment put up blistering growth in the quarter, advancing 24.3% year-over-year to $345 million.

It now represents 27% of the company’s total net revenue. All the while, the legacy Core Business Services segment grew 1.4% over the year-ago period to $951 million for the quarter.

Genpact’s adjusted diluted EPS jumped 16.7% year-over-year to $0.98 during the quarter. This topped the analyst consensus in the quarter by $0.06.

Click here to download our most recent Sure Analysis report on G (preview of page 1 of 3 below):

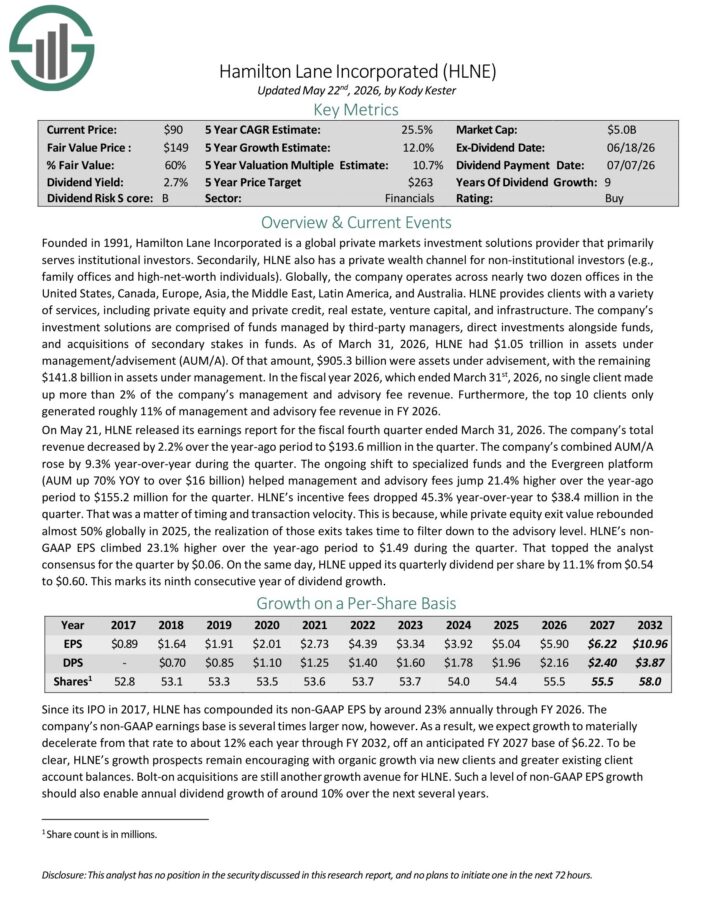

Beaten Down Dividend Stock #3: Hamilton Lane (HLNE)

Expected Total Return: 30.6%

Hamilton Lane Incorporated is a global private markets investment solutions provider that primarily serves institutional investors.

Secondarily, HLNE also has a private wealth channel for non-institutional investors (e.g., family offices and high-net-worth individuals). Globally, the company operates across nearly two dozen offices in the United States, Canada, Europe, Asia, the Middle East, Latin America, and Australia.

HLNE provides clients with a variety of services, including private equity and private credit, real estate, venture capital, and infrastructure.

On May 21, HLNE released its earnings report for the fiscal fourth quarter ended March 31, 2026. The company’s total revenue decreased by 2.2% over the year-ago period to $193.6 million in the quarter.

The company’s combined AUM/A rose by 9.3% year-over-year during the quarter.

The ongoing shift to specialized funds and the Evergreen platform (AUM up 70% YOY to over $16 billion) helped management and advisory fees jump 21.4% higher over the year-ago period to $155.2 million for the quarter.

HLNE’s incentive fees dropped 45.3% year-over-year to $38.4 million in the quarter. That was a matter of timing and transaction velocity.

On the same day, HLNE upped its quarterly dividend per share by 11.1% from $0.54 to $0.60. This marks its ninth consecutive year of dividend growth.

Click here to download our most recent Sure Analysis report on HLNE (preview of page 1 of 3 shown below):

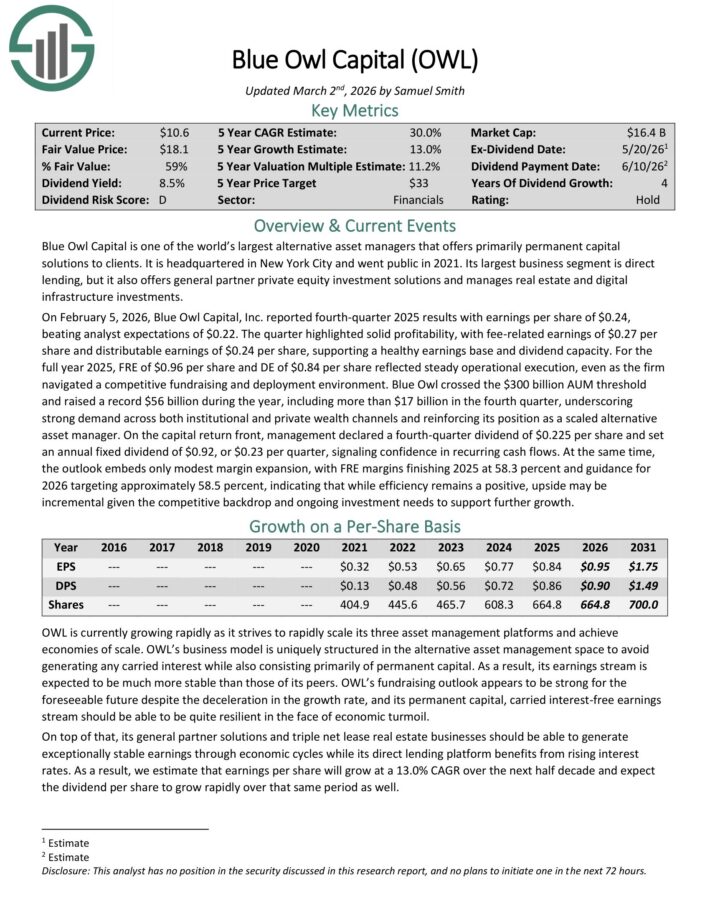

Beaten Down Dividend Stock #2: Blue Owl Capital (OWL)

Expected Total Return: 32.8%

Blue Owl Capital is one of the world’s largest alternative asset managers that offers primarily permanent capital solutions to clients.

It is headquartered in New York City and went public in 2021. Its largest business segment is direct lending, but it also offers general partner private equity investment solutions and manages real estate and digital infrastructure investments.

On February 5, 2026, Blue Owl Capital, Inc. reported fourth-quarter 2025 results with earnings per share of $0.24, beating analyst expectations of $0.22.

Fee-related earnings were $0.27 per share and distributable earnings were $0.24 per share, supporting a healthy earnings base and dividend capacity.

For the full year 2025, FRE of $0.96 per share and DE of $0.84 per share reflected steady operational execution, even as the firm navigated a competitive fundraising and deployment environment.

Click here to download our most recent Sure Analysis report on OWL (preview of page 1 of 3 shown below):

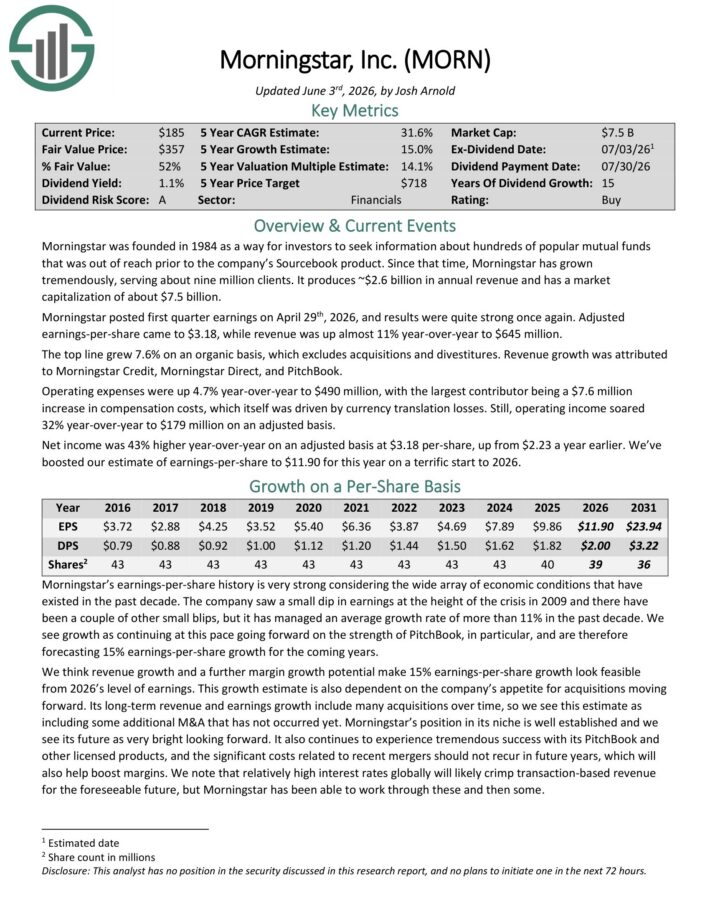

Beaten Down Dividend Stock #1: Morningstar Inc. (MORN)

Expected Total Return: 38.6%

Morningstar serves about nine million clients and produces ~$2.6 billion in annual revenue.

Morningstar posted first quarter earnings on April 29th, 2026, and results were quite strong once again. Adjusted earnings-per-share came to $3.18, while revenue was up almost 11% year-over-year to $645 million.

The top line grew 7.6% on an organic basis, which excludes acquisitions and divestitures. Revenue growth was attributed to Morningstar Credit, Morningstar Direct, and PitchBook.

Operating expenses were up 4.7% year-over-year to $490 million, with the largest contributor being a $7.6 million increase in compensation costs, which itself was driven by currency translation losses.

Still, operating income soared 32% year-over-year to $179 million on an adjusted basis.

Net income was 43% higher year-over-year on an adjusted basis at $3.18 per-share, up from $2.23 a year earlier. We’ve boosted our estimate of earnings-per-share to $11.90 for this year.

Click here to download our most recent Sure Analysis report on MORN (preview of page 1 of 3 shown below):

Other Blue Chip Stock Resources

The resources below will give you a better understanding of dividend growth investing:

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

")

")

{kind=link}