El Salvador’s Bitcoin reserve is back in the market spotlight because its public one-BTC-a-day narrative has resurfaced just as Bitcoin’s drawdown, IMF conditions, and wallet-accounting questions are pressing on the same policy.

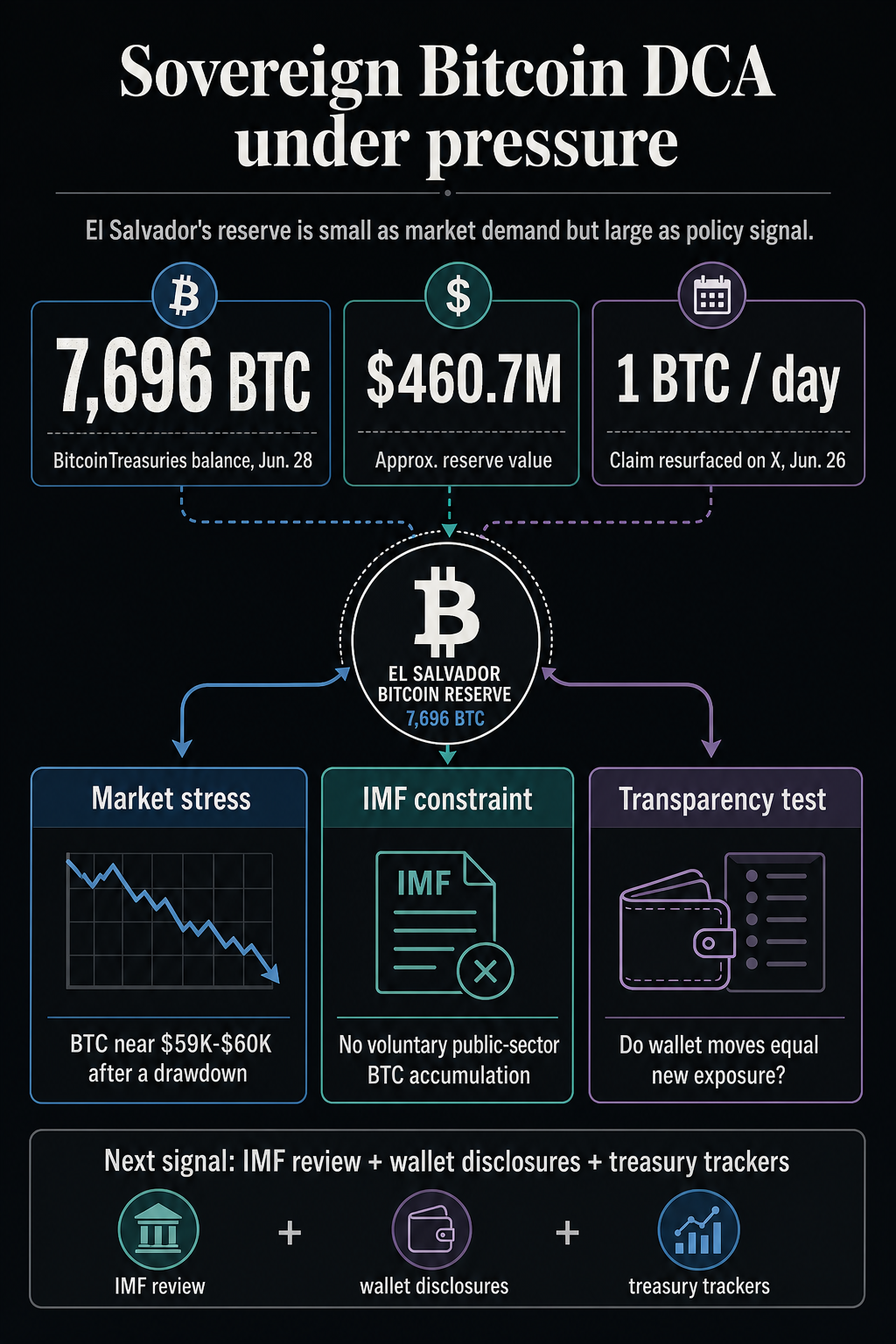

BitcoinTreasuries lists El Salvador’s government holdings at 7,696 BTC, worth about $460 million, as of Jun. 28. The figure keeps the country among the largest government-linked Bitcoin holders tracked by the site and gives the renewed debate over its one-Bitcoin-a-day strategy a concrete anchor.

The market backdrop gives that debate urgency. CryptoSlate’s Bitcoin market page showed BTC changing hands around the $59,000 to $60,000 range, after a high-single-digit decline over seven days and an almost 19% drop over 30 days.

The result is a durability test for sovereign accumulation. A daily one-BTC allocation is too small to move the global Bitcoin market on its own, yet it can still indicate whether government dollar-cost averaging behaves differently from ETF demand or corporate treasury demand when the same asset is falling.

Why a small reserve carries large policy weight

Measured against Bitcoin’s roughly $1.2 trillion market value, El Salvador’s 7,696 BTC reserve is a limited market position. It represents a fraction of the Bitcoin supply and is dwarfed by the holdings held by US spot Bitcoin ETFs, exchanges, and the largest corporate treasury buyers.

Measured against sovereign policy, the reserve carries more weight. It is a continuing political signal, a fiscal accounting question, and a test of how far a government can carry a Bitcoin strategy after retreating from the most aggressive version of its legal-tender experiment.

That distinction separates El Salvador from better-known institutional Bitcoin flows. ETF investors can redeem shares. Corporate holders can refinance, issue equity, cut spending, or face pressure from public-market investors.

A government reserve sits inside a different system. It has to coexist with budget targets, external lenders, public accounting, and, in El Salvador’s case, a formal IMF program.

ElementWhat is establishedEditorial weightReserve balanceBitcoinTreasuries listed El Salvador at 7,696 BTC, worth about $460.7 million.The reserve remains visible during a drawdown and provides a current balance-sheet anchor.Daily-buying narrativeA June 26 X post by Pete Rizzo resurfaced claims that El Salvador buys 1 BTC per day and had bought more than 170 BTC in 2026.The post explains why the issue returned to market discussion and should be treated as social context, with net accumulation assessed against wallet and IMF records.IMF constraintIMF materials describe commitments around voluntary Bitcoin use, US-dollar tax payments, and no voluntary public-sector BTC accumulation.The policy tension turns the reserve into an accounting and credibility test, alongside its role as a Bitcoin conviction trade.

The table also shows the core ambiguity. El Salvador can keep a Bitcoin reserve in the public eye, while the IMF record focuses on the overall public-sector Bitcoin stock and the conditions attached to an Extended Fund Facility. The durability test lives in that gap.

IMF conditions changed the Bitcoin policy backdrop

El Salvador’s original Bitcoin policy was built around public adoption, legal-tender status, and a president willing to turn BTC purchases into a national brand. The latter IMF program changed the operating environment.

In a March 2025 press briefing, the IMF said reforms had made Bitcoin acceptance voluntary in the private sector, made taxes payable only in US dollars, and committed the government to avoiding the accumulation of Bitcoin at the overall public-sector level.

The fund’s first review materials then put sharper mechanics around that approach, including a continuous quantitative performance criterion with a zero ceiling on voluntary BTC accumulation by the public sector and a zero ceiling on public-sector BTC-denominated or BTC-indexed debt and tokenized instruments.

That language leaves El Salvador’s Bitcoin reserve in place while changing how it must be understood.

Before the IMF program, a public one-BTC-a-day pledge could be understood mostly as political signaling and Bitcoin accumulation. After the program, the same public message appears next to the program criteria that assess whether the public sector is voluntarily increasing exposure.

The question now is whether visible reserve increases, daily purchase claims, and wallet movements add net public-sector BTC, or whether they are accounting movements inside an already committed stock.

CryptoSlate previously reported that the IMF characterized apparent increases in El Salvador’s Strategic Bitcoin Reserve Fund as consolidation across government-owned wallets rather than new accumulation by the public sector as a whole.

That distinction is technical but central. A reserve can appear larger in one public-facing wallet or tracker without necessarily violating a no-accumulation commitment, provided the underlying public-sector stock remains unchanged.

El Salvador still wants to be seen as a Bitcoin country. The unresolved issue is whether the public signal, wallet accounting, and IMF program conditions can continue to align as Bitcoin prices fall and scrutiny rises.

Sovereign DCA has its own stress points

The market backdrop shows how other Bitcoin demand channels are reacting under stress.

CryptoSlate recently reported roughly $5.94 billion in US spot Bitcoin ETF outflows over six straight weeks, raising the question of whether the ETF complex had just seen its first real capitulation event.

In another corner of the institutional trade, Strategy’s Bitcoin financing model has come under pressure as parts of its capital stack weakened.

Those developments are secondary to El Salvador’s case, but they create a useful contrast. ETF demand can cool quickly when investors pull cash. Corporate treasury demand can become a financing story when market confidence weakens.

Sovereign accumulation differs because the constraints include political permission, external financing, fiscal credibility, and the ability to explain the accounting.

That can make sovereign DCA more durable in one sense and more fragile in another.

It can be more durable because a government is insulated from daily ETF redemption flows and from the same public-market financing channel as a listed company.

If the daily BTC allocation is small enough, the direct cash burden can remain modest compared with the broader fiscal program.

It can also be more fragile because the policy is harder to separate from national credibility. When a country is operating under IMF conditions, a symbolic Bitcoin reserve becomes a public test of program discipline as well as a bet on future price.

It becomes part of how lenders, markets, and citizens judge whether the government is following the program it agreed to.

A rally can make almost any accumulation strategy look disciplined after the fact. A drawdown tests whether the policy has institutional depth or depends on momentum, opaque accounting, and political capital.

The next test is transparency

The current record shows that El Salvador’s Bitcoin strategy remains a durable signal. The reserve is still tracked, the one-BTC-a-day narrative still travels on X, and the country continues to occupy a unique place in Bitcoin’s sovereign adoption history.

If El Salvador can show that reserve movements, public messaging, and IMF conditions are consistent with one another, then the strategy can survive as a contained sovereign Bitcoin position even during a drawdown.

In that scenario, the daily-buying narrative remains politically valuable while the fiscal program limits the risk to the broader public sector.

If it cannot, the signal changes. A Bitcoin reserve that looked like disciplined sovereign DCA could become an accounting dispute with a lender whose program is meant to stabilize public finances.

The market impact of one BTC per day would still be tiny, but the policy impact could be much larger.

That is the difference between a government reserve and a private balance sheet. ETF investors can leave. Corporate buyers can restructure. A sovereign Bitcoin strategy must remain legible to creditors, citizens, and markets simultaneously.

For now, El Salvador’s Bitcoin reserve is best understood as a live policy stress test.

The next meaningful signal is whether the next IMF review, public wallet disclosures, and treasury trackers continue to point to a consistent accounting picture. That is where the durability of sovereign Bitcoin DCA will be tested.

")

{kind=link}