AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Stock $63.93 (-12.7%)

EPS YoY +160.0%|Rev YoY +7.4%|Net Margin -3.6%

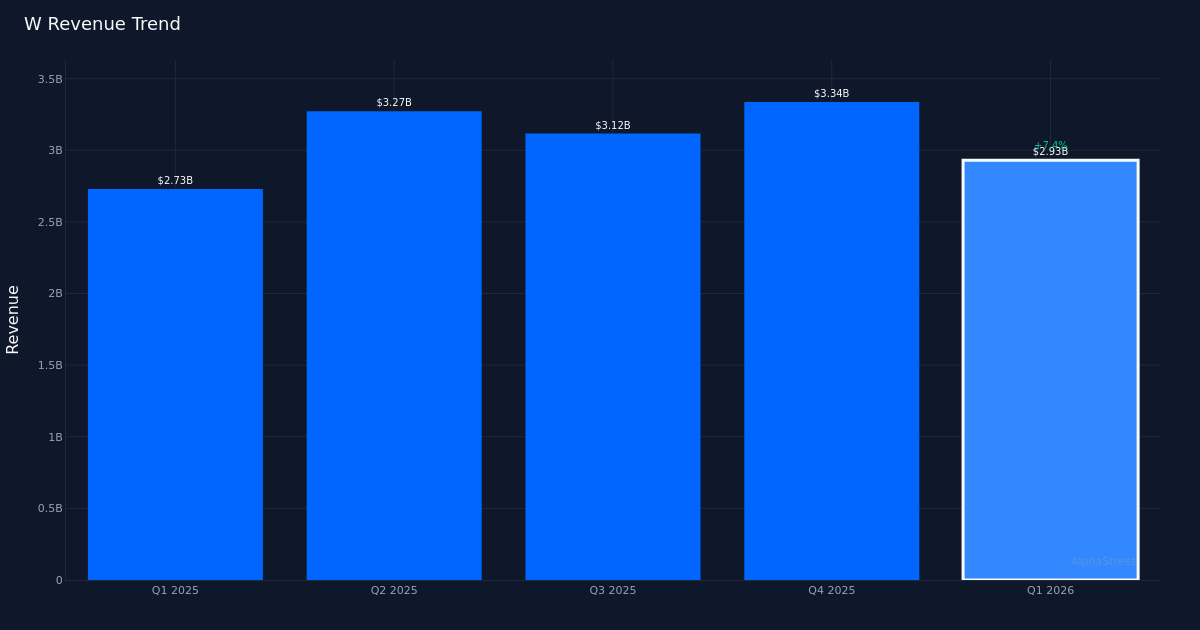

Wayfair’s (W) return to profitability momentum hit a speed bump in Q1 2026, as the online furniture retailer missed earnings expectations despite posting solid revenue growth. The company reported adjusted EPS of $0.26, falling short of the $0.27 consensus estimate by 3.7%, though this still represented a 160.0% improvement from the year-ago quarter’s $0.10. Revenue climbed 7.4% year-over-year to $2.93B, but the miss on the bottom line triggered a sharp 12.7% selloff that pushed shares to $63.93, suggesting investors remain hypersensitive to any deceleration in the turnaround narrative.

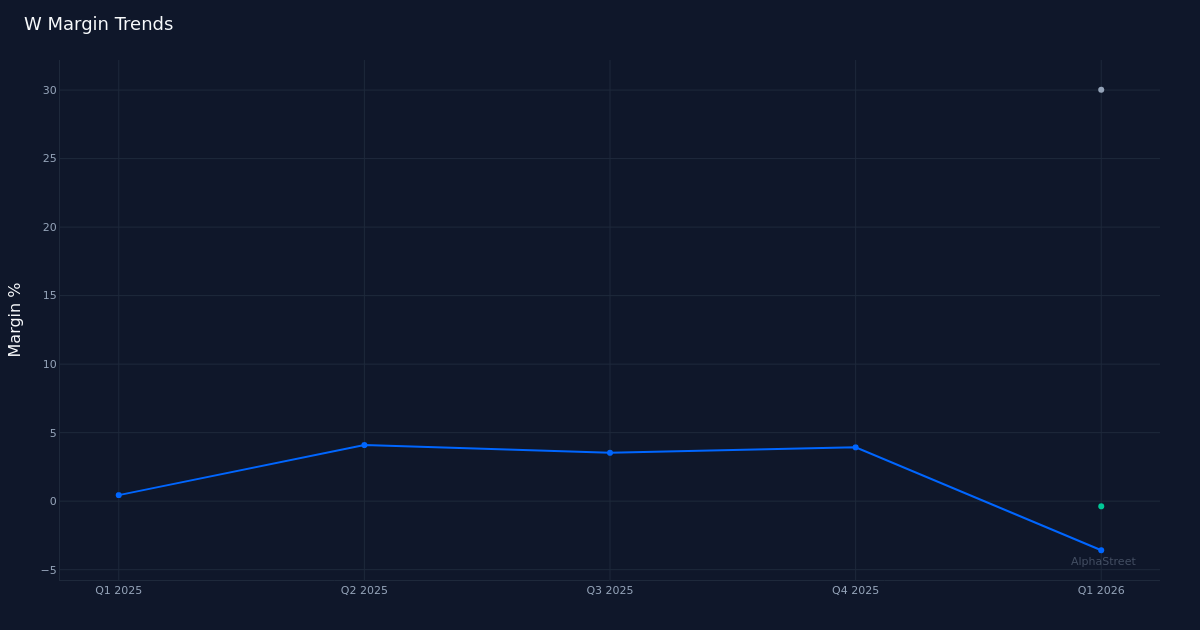

The quality of earnings deteriorated meaningfully from a profitability perspective, raising questions about the sustainability of Wayfair’s margin expansion story. Net loss for the quarter was $105.0M, compared to a loss of $113M last year. Operating margin similarly turned negative at -0.4%. The gross margin of 30.0% held relatively stable, indicating that profitability pressure is manifesting further down the income statement through elevated operating expenses rather than pricing or product mix deterioration.

Management attempted to reframe the narrative around adjusted EBITDA performance, where results appeared stronger on the surface. The company reported $151.0M of adjusted EBITDA, which management characterized positively in their commentary: “Our 5.2% adjusted EBITDA margin in the first quarter is the best Q1 result we’ve delivered in five years, and it approaches what we reported in the first quarter of 2021.” This framing highlights the disconnect between adjusted metrics that management prefers to emphasize and the GAAP profitability that actually determines shareholder value creation. The gap between $151.0M in EBITDA and $11.0M in operating loss suggests substantial non-cash charges or adjustments that warrant scrutiny.

The revenue trajectory reveals a meaningful deceleration from the robust growth rates achieved in the back half of 2025. The four-quarter trend shows Q1 2026 revenue of $2.93B following Q4 2025’s $3.34B, Q3 2025’s $3.12B, and Q2 2025’s $3.27B. While some sequential decline from Q4 to Q1 reflects normal seasonality in the home goods category, the 7.4% year-over-year growth rate in Q1 marks a potential inflection point. Management attributed this to balanced drivers: “Our net revenue grew by 7% in the first quarter, driven by order growth of 3% and AOV expansion of 4%.” The composition matters here—with order growth of just 3% barely outpacing the 1.4% active customer growth to 21.4 million active customers, Wayfair is increasingly dependent on extracting more revenue per transaction rather than meaningfully expanding its customer base.

The customer metrics expose a fundamental challenge to the growth algorithm that should concern long-term investors. Active customer growth of 1.4% represents minimal expansion of the addressable pool, suggesting that market share gains are proving difficult despite Wayfair’s scale advantages in online furniture retail. The 3% order growth implies existing customers are purchasing slightly more frequently, while the 4% average order value expansion indicates either price increases, mix shift toward higher-ticket items, or attach rate improvements. This reliance on intensifying monetization of a slowly growing customer base creates vulnerability if macroeconomic headwinds reduce consumer willingness to make discretionary home purchases.

Cash generation metrics provided the quarter’s clearest bright spot, with free cash flow substantially exceeding net income. The company’s free cash flow was negative $106.0M in Q1, while operating cash flow came in at $52.0M. Positive cash generation provides Wayfair with financial flexibility to invest in growth initiatives or weather potential demand softness without liquidity concerns.

Forward guidance commentary suggests management sees persistent headwinds that may pressure near-term results. During the analyst Q&A, Peter Keith noted: “… just to parse out the guidance for mid single digit revenue growth in Q2, it does sound like the industry has stepped down and gotten a little bit worse in April.” This acknowledgment of April weakness entering Q2 indicates that the 7.4% growth achieved in Q1 may represent a high-water mark for 2026 rather than a sustainable baseline. The implied mid-single-digit growth guidance for Q2 would represent further deceleration, making it increasingly difficult to achieve the ambitious targets management has previously articulated.

The disconnect between management’s long-term aspirations and near-term execution became more apparent in the quarter’s commentary. Management referenced in their shareholder letter “a 20% plus organic growth rate that you guys are targeting,” creating a stark contrast with the current 7.4% reality and the softer outlook for Q2. This gap between vision and delivery explains the severity of the stock reaction—investors appear to be recalibrating expectations around the timeline and probability of reaching those ambitious growth targets. The furniture and home goods category remains inherently cyclical and sensitive to housing market dynamics, making sustained double-digit growth challenging without significant market share capture or category expansion.

The margin commentary around gross profit evolution added another layer of uncertainty to the forward outlook. Management stated: “Gross margin for the first quarter was 30.1% of net revenue I talked at length in February about how the componentry of gross margin will evolve over 2026.” This cryptic reference to evolving margin composition without providing specifics suggests potential headwinds that management is pre-emptively framing, whether from promotional intensity, shipping costs, or product mix shifts. The 30.0% gross margin achieved in Q1 establishes a baseline, but without clarity on the expected trajectory, investors face uncertainty around whether operating leverage will materialize as revenue scales.

What to Watch: Q2 revenue growth will be critical to assess whether the April softness proves transitory or signals a more sustained demand headwind. Active customer acquisition trends need to reaccelerate above the 1.4% rate to support a credible path to management’s long-term growth targets. Gross margin evolution through the remainder of 2026 will determine whether operating leverage can drive margin expansion or if the current negative operating margin persists. Finally, any commentary around promotional intensity or competitive dynamics in online furniture retail will help clarify whether Wayfair’s growth challenges are company-specific execution issues or broader industry headwinds.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

{kind=link}